simply amazing, always for you.

When Salary Day Feels Like a Reset Button

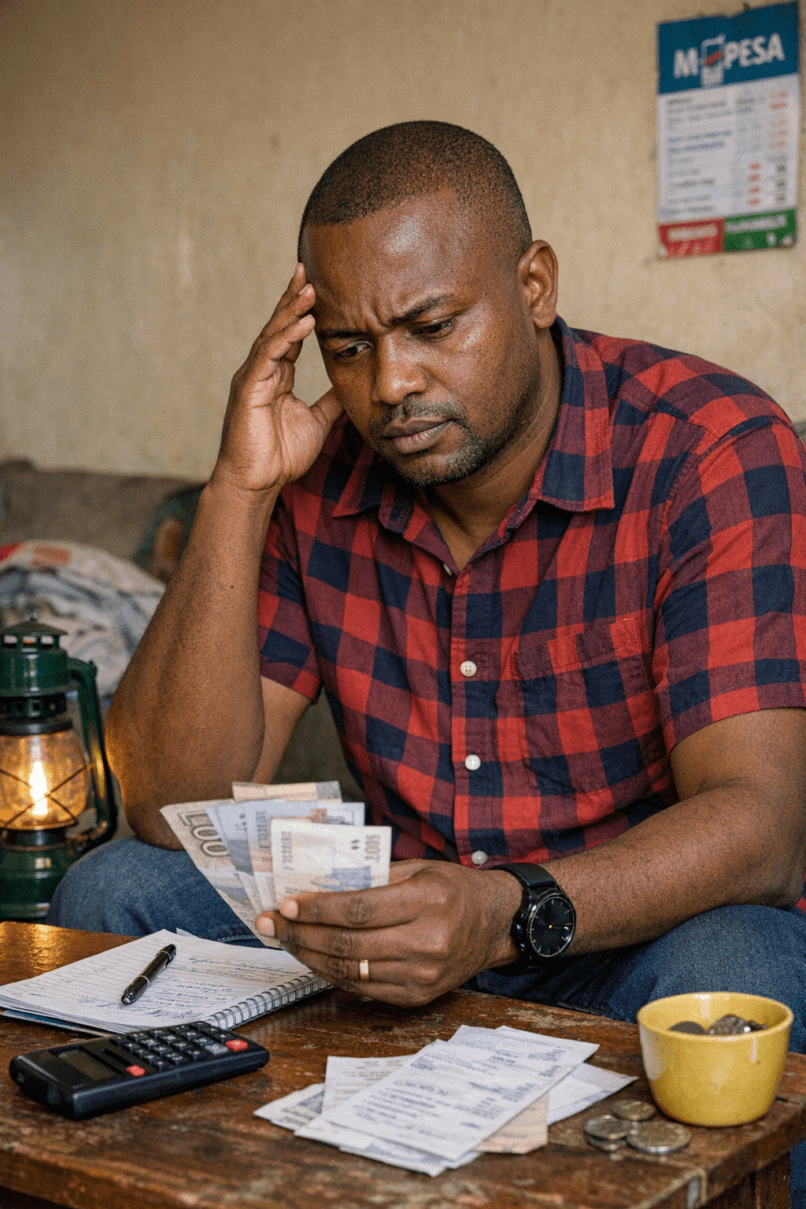

For millions of working Kenyans, payday is not a celebration. It is a reset.

The salary comes in. Rent is paid. School fees are cleared. Electricity tokens are bought. A few debts are settled. Groceries are restocked. Transport is budgeted.

And just like that, the money is gone.

By mid-month, the anxiety begins. By the third week, the borrowing starts. By the fourth week, survival mode kicks in.

Living paycheck to paycheck in Kenya has become the financial norm — not just for low-income earners, but for middle-class professionals, small business owners, and even salaried workers in respected careers. The pressure is relentless.

This is not just a personal finance issue. It is a structural, cultural, and economic reality.

In this in-depth SEO-optimized guide, we will break down:

- Why so many Kenyans live paycheck to paycheck

- The hidden economic and social drivers behind it

- The psychological cost of financial instability

- And most importantly, practical, realistic solutions you can apply immediately

If you feel like your income disappears faster than you can control it, this article is for you.

What Does Living Paycheck to Paycheck Really Mean?

Living paycheck to paycheck means:

- You rely entirely on your next salary to survive.

- You have little or no savings.

- Any emergency (hospital bill, funeral contribution, job loss) can push you into debt.

- You regularly borrow before your next payday.

It does not necessarily mean you are poor.

It means you lack a financial buffer.

In Kenya’s context, it often looks like:

- Using mobile loans to survive the last week of the month.

- Delaying rent until the landlord reminds you.

- Asking friends for short-term loans.

- Borrowing from chamas or SACCOs to cover daily expenses instead of investments.

Why Are So Many Kenyans Living Paycheck to Paycheck?

Let’s break down the real causes.

1. Rising Cost of Living vs. Stagnant Wages

Kenya’s cost of living has steadily increased over the years.

Food prices fluctuate constantly. Fuel prices influence transport costs. Electricity tariffs shift. Rent in major cities continues to rise.

In urban centers like Nairobi, housing alone can take 30–50% of income for middle-class earners.

But wages? They have not grown at the same pace.

This gap between income growth and expense growth is the first major driver of financial strain.

When your salary remains constant but expenses rise annually, your purchasing power shrinks.

2. Overdependence on Debt and Mobile Loans

Kenya’s digital finance ecosystem is one of the most advanced in Africa, largely driven by Safaricom and its mobile money platform M-Pesa.

While revolutionary, this ecosystem has also made borrowing dangerously easy.

Mobile loan apps offer:

- Instant approval

- No paperwork

- Fast disbursement

But often:

- High interest rates

- Short repayment windows

- Heavy penalties

The result?

Many Kenyans are caught in a debt cycle:

Borrow → Repay → Borrow again → Repeat.

Instead of loans funding business growth, they fund survival.

3. Informal Employment and Income Instability

A significant percentage of Kenya’s workforce operates in the informal sector.

This includes:

- Boda boda riders

- Market traders

- Casual laborers

- Freelancers

- Small business owners

Income in these sectors is unpredictable.

One good week does not guarantee another.

Without stable cash flow, budgeting becomes guesswork.

And when income fluctuates, savings become inconsistent.

4. Social and Cultural Financial Pressure

Kenyan society is community-driven.

There are expectations:

- Contributing to funerals (harambee)

- Supporting extended family

- Attending weddings and ceremonies

- Sending money “upcountry”

While these traditions strengthen bonds, they can weaken personal finances.

Many people overspend to avoid social embarrassment.

Some prioritize social appearance over financial stability.

This pressure silently drains income.

5. Lack of Financial Literacy

Financial education is rarely taught in schools.

Most Kenyans learn about money through:

- Observation

- Trial and error

- Mistakes

Few understand:

- Compound interest

- Asset vs. liability

- Emergency fund principles

- Investment diversification

Without knowledge, income — no matter how high — can disappear.

6. Lifestyle Inflation

As income increases, expenses increase too.

New job? Move to a bigger apartment.

Salary raise? Upgrade the car.

Bonus? New phone.

Instead of building savings when income rises, lifestyle expands.

This is called lifestyle inflation — and it keeps many middle-class Kenyans financially fragile.

The Psychological Cost of Living Paycheck to Paycheck

Financial stress affects more than your wallet.

It affects:

- Mental health

- Relationships

- Work productivity

- Self-esteem

Constant money anxiety creates:

- Sleepless nights

- Irritability

- Poor decision-making

When survival mode becomes permanent, long-term planning disappears.

And without long-term thinking, wealth building becomes impossible.

How to Break the Paycheck-to-Paycheck Cycle in Kenya

Now the practical part.

No theory. No fluff. Just actionable solutions.

1. Master Cash Flow Before Anything Else

You cannot fix what you do not measure.

Track every shilling for 30 days.

Categorize spending:

- Rent

- Food

- Transport

- Debt repayment

- Entertainment

- Family support

Once you see the data, patterns become obvious.

Financial clarity is the first breakthrough.

2. Build a Micro Emergency Fund

You don’t need millions.

Start with KSh 5,000.

Then aim for KSh 20,000.

Eventually, build up to 3 months of expenses.

This buffer protects you from:

- Medical emergencies

- Job delays

- Unexpected travel

- Urgent repairs

Emergency funds stop you from borrowing.

3. Eliminate High-Interest Debt First

If you have mobile loans, prioritize clearing them.

Use the debt avalanche method:

- Pay minimums on all debts

- Attack the highest interest loan aggressively

Once cleared, redirect that money to savings.

Debt elimination is financial oxygen.

4. Increase Income Strategically

Sometimes cutting expenses is not enough.

You need to increase income.

Options include:

- Freelancing online

- Starting a small side business

- Upskilling into higher-paying industries

- Negotiating salary

Even an extra KSh 5,000–10,000 per month can transform your savings rate.

5. Automate Savings Immediately After Payday

Do not save what is left.

Save first.

The day salary enters your account:

- Transfer a fixed percentage to savings

- Treat it like rent — non-negotiable

Automation removes emotion.

6. Avoid Lifestyle Upgrades Until You Have Stability

Before upgrading:

- Have 3–6 months of savings

- Be debt-free (except long-term investments)

- Have a clear investment plan

Status purchases are temporary.

Financial freedom is permanent.

7. Join the Right Financial Community

Chamas and SACCOs can be powerful tools — if used correctly.

Invest in:

- Income-generating assets

- Land

- Business ventures

Avoid using group savings to fund consumption.

Structural Solutions Kenya Needs

While personal discipline matters, systemic changes are also necessary:

- Better job creation policies

- Regulation of digital lending

- Financial literacy in schools

- Affordable housing initiatives

Economic resilience requires both individual action and national strategy.

The Hard Truth: Income Alone Will Not Save You

Many people believe:

“If I earn more, I will stop struggling.”

But high income without financial discipline still leads to paycheck-to-paycheck living.

Financial stability is built on:

- Spending less than you earn

- Investing consistently

- Avoiding unnecessary debt

- Planning long-term

Income helps — but habits determine outcomes.

From Survival to Stability

Living paycheck to paycheck in Kenya is common — but it does not have to be permanent.

The shift begins with:

- Awareness

- Discipline

- Strategy

- Long-term thinking

Financial freedom is not about earning millions overnight.

It is about building margin between your income and expenses — and protecting that margin relentlessly.

You don’t need perfection.

You need a plan — and the courage to stick to it.

SUGGESTED READS

- Why More Kenyans Are Choosing Side Hustles Over Employment

- How to Manage Money in Kenya When Prices Keep Rising

- The Honest Reality of Freelancing in Kenya (Income, Struggles, and Success Tips)

- The Dark Side of Hustling in Kenya: What Social Media Never Shows You

- How Young Kenyans Are Surviving Without Stable Jobs

- “Your Goods Are Expensive” — The Lie, the Truth, and the Fix

- Why Wait for Employment? Build a Profitable Business from Home in Kenya

Support Our Website!

We appreciate your visit and hope you find our content valuable. If you’d like to support us further, please consider contributing through the TILL NUMBER: 9549825. Your support helps us keep delivering great content!

If you’d like to support Nabado from outside Kenya, we invite you to send your contributions through trusted third-party services such as Remitly, western union, SendWave, or WorldRemit. These platforms are reliable and convenient for international money transfers.

Please use the following details when sending your support:

Phone Number: +254701838999

Recipient Name: Peterson Getuma Okemwa

We sincerely appreciate your generosity and support. Thank you for being part of this journey!